Product Life Cycle Accounting and Reporting Standard

Status::

Links:: Carbon Accounting GHG Protocol

Metadata

Authors:: World Resources Institute,

Title:: Product Life Cycle Accounting and Reporting Standard

Date:: 2011

Publisher:: World Resources Institute

URL:: https://ghgprotocol.org/product-standard

DOI::

World Resources Institute. (2011). Product Life Cycle Accounting and Reporting Standard. World Resources Institute. https://ghgprotocol.org/product-standard

Notes & Annotations

Color-coded highlighting system used for annotations

📑 Annotations (imported on 2024-03-09#11:47:21)

The GHG Protocol Product Life Cycle Accounting and Reporting Standard (referred to as the Product Standard) provides requirements and guidance for companies and other organizations to quantify and publicly report an inventory of GHG emissions and removals associated with a specific product. The primary goal of this standard is to provide a general framework for companies to make informed choices to reduce greenhouse gas emissions from the products (goods or services) they design, manufacture, sell, purchase, or use.

Companies must be able to understand and manage their product-related GHG risks if they are to ensure long-term success in a competitive business environment and be prepared for any future product-related programs and policies.

This standard focuses on emissions and removals generated during a product’s life cycle and does not address avoided emissions or actions taken to mitigate released emissions.

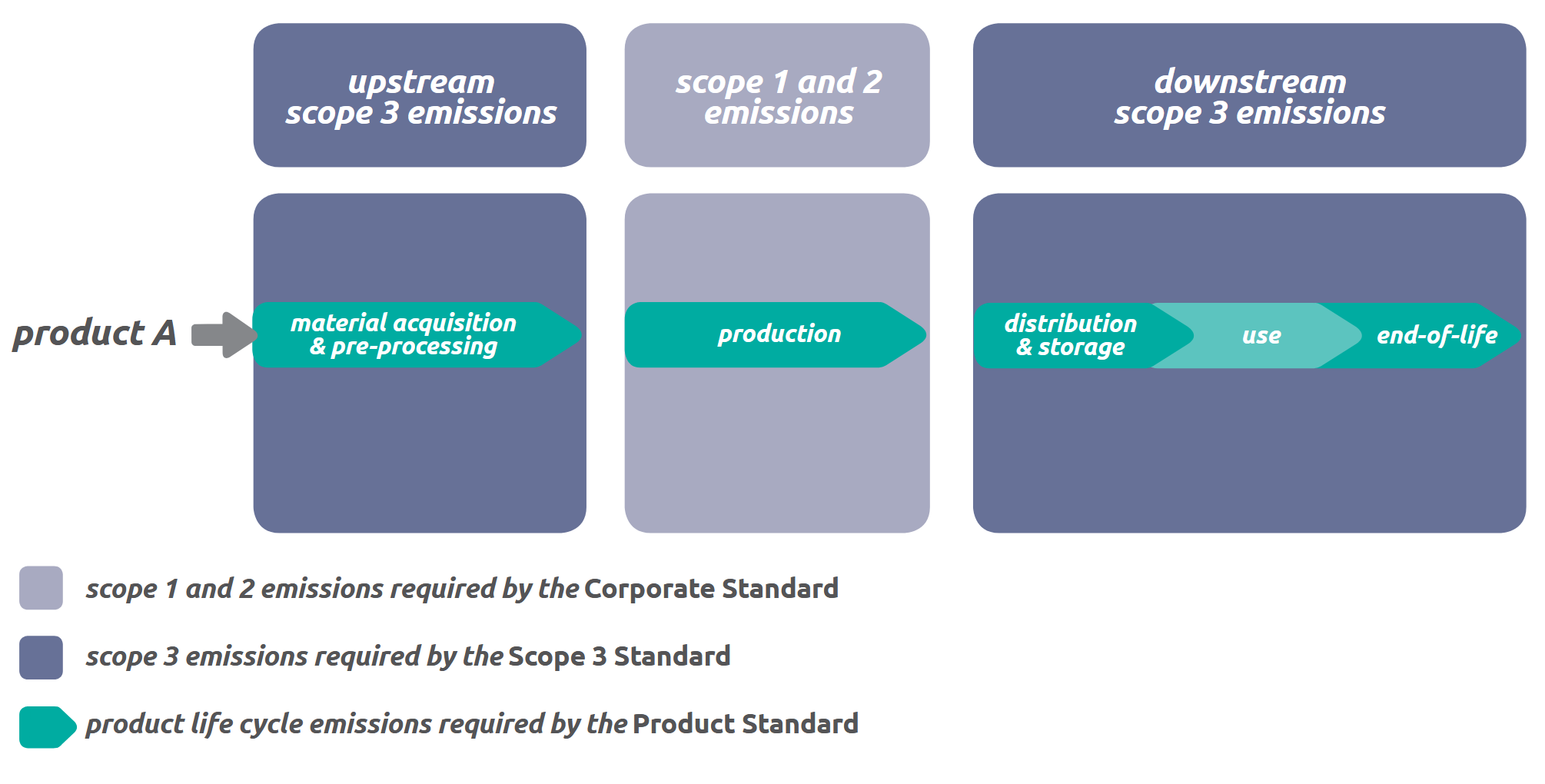

The GHG Protocol Scope 3 Standard and GHG Protocol Product Standard both take a value chain or life cycle approach to GHG accounting and were developed simultaneously. The Scope 3 Standard builds on the GHG Protocol Corporate Standard and accounts for value chain emissions at the corporate level, while the Product Standard accounts for life cycle emissions at the individual product level. Together, the three standards provide a comprehensive approach to value chain GHG measurement and management.

The sum of the life cycle emissions of each of a company’s products, combined with additional scope 3 categories (e.g., employee commuting, business travel, and investments), should approximate the company’s total corporate GHG emissions (i.e., scope 1 + scope 2 + scope 3). In practice, companies are not expected or required to calculate life cycle inventories for individual products when calculating scope 3 emissions.

The relationship between the Corporate, Scope 3, and Product Standards for a company manufacturing product A

The Product Standard accounts for the GHG emissions and removals that occur during a product’s life cycle. A product assessment limited to only GHGs has the benefit of simplifying the analysis and producing results that can be clearly communicated to stakeholders. The limitation of a GHG-only inventory is that potential trade-offs or cobenefits between environmental impacts can be missed. Therefore, the results of a GHG-only inventory should not be used to communicate the overall environmental performance of a product. Non-GHG environmental impacts that occur during the life cycle of a product should also be considered when making decisions to reduce GHG emissions based on the inventory results. Examples of potentially significant non-GHG impacts for some products include ecosystem degradation, resource depletion, ozone depletion, and negative human health impacts.

The Product Standard builds on the framework and requirements established in the ISO LCA standards (14040:2006, Life Cycle Assessment: Principles and Framework and 14044:2006, Life Cycle Assessment: Requirements and Guidelines) and PAS 2050, with the intent of providing additional specifications and guidance to facilitate the consistent quantification and public reporting of product life cycle GHG inventories.

Product GHG inventories,4 also commonly known as product carbon footprints, are a subset of LCA because they focus only on the climate change impact category (the limitations of which are discussed in chapter 1). However, the accounting methodologies and requirements presented in this standard follow the life cycle approach as established by ISO LCA standards 14040 and 14044.

Companies shall account for carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), sulfur hexafluoride (SF6), perfluorocarbons (PFCs), and hydrofluorocarbons (HFCs) emissions to, and removals from, the atmosphere. Additional GHGs included in the inventory shall be listed in the inventory report.

📑 Annotations (imported on 2024-03-17#07:13:43)

The Product Standard is intended to support performance tracking of a product’s GHG inventory and emissions reductions over time. Additional prescriptiveness on the accounting methodology, such as allocation choices and data sources, are needed for product labeling, performance claims, consumer and business decision making based on comparison of two or more products, and other types of product comparison based on GHG impacts.

Claims regarding the overall environmental superiority or equivalence of one product versus a competing product, referred to in ISO 14044 as comparative assertions, are not supported by the Product Standard.