Corporate Value Chain (Scope 3) Accounting and Reporting Standard

Status:: 🟩

Links:: GHG Protocol

Metadata

Authors:: World Resources Institute,

Title:: Corporate Value Chain (Scope 3) Accounting and Reporting Standard

Date:: 2011

Publisher:: World Resources Institute

URL:: https://ghgprotocol.org/corporate-value-chain-scope-3-standard

DOI::

World Resources Institute. (2011). Corporate Value Chain (Scope 3) Accounting and Reporting Standard. World Resources Institute. https://ghgprotocol.org/corporate-value-chain-scope-3-standard

Notes & Annotations

Color-coded highlighting system used for annotations

📑 Annotations (imported on 2024-03-17#07:14:09)

The GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard (also referred to as the Scope 3 Standard) provides requirements and guidance for companies and other organizations to prepare and publicly report a GHG emissions inventory that includes indirect emissions resulting from value chain activities (i.e., scope 3 emissions).

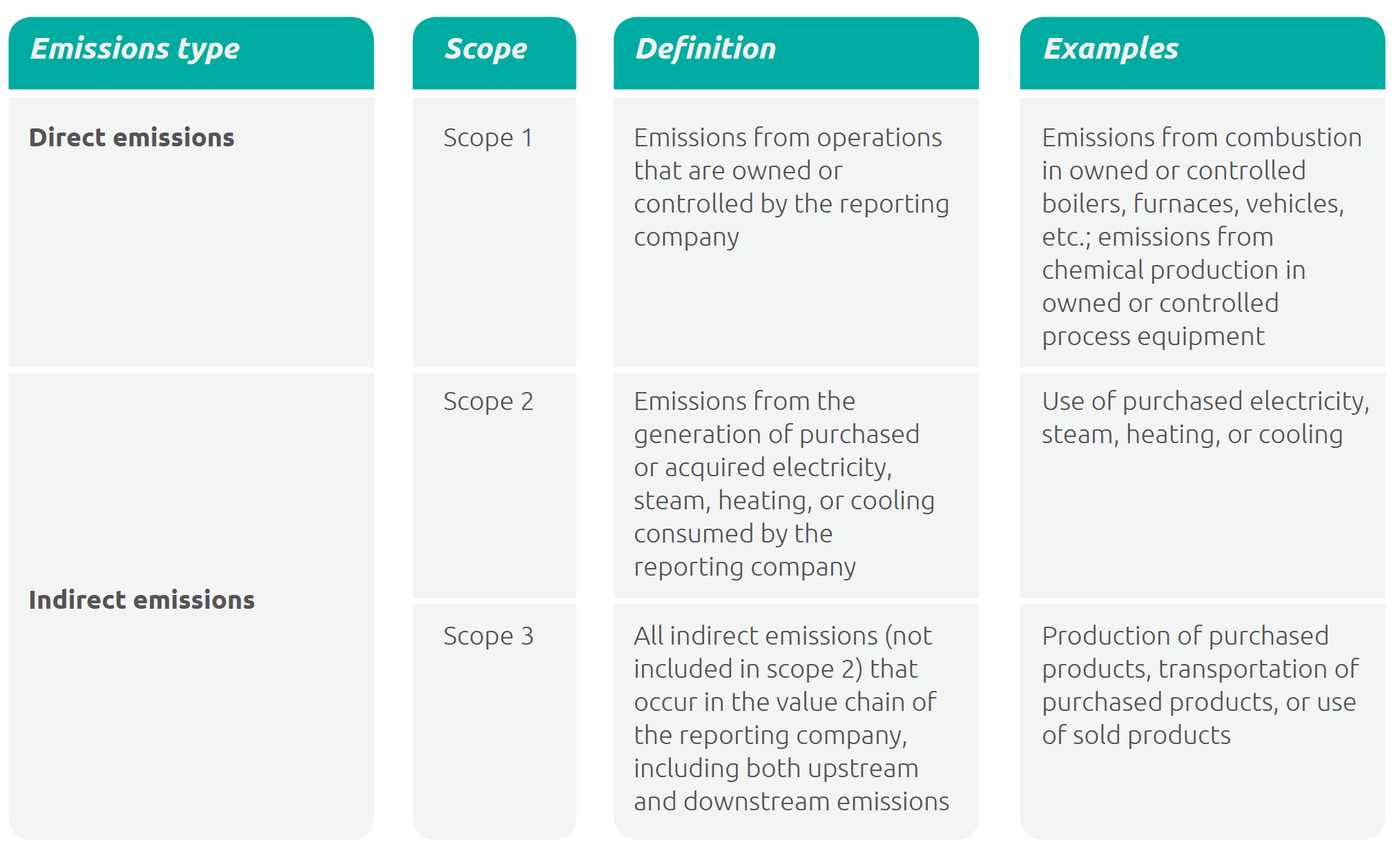

The Corporate Standard classifies a company’s direct and indirect GHG emissions into three “scopes,” and requires that companies account for and report all scope 1 emissions (i.e., direct emissions from owned or controlled sources) and all scope 2 emissions (i.e., indirect emissions from the generation of purchased energy consumed by the reporting company). The Corporate Standard gives companies flexibility in whether and how to account for scope 3 emissions (i.e., all other indirect emissions that occur in a company’s value chain).

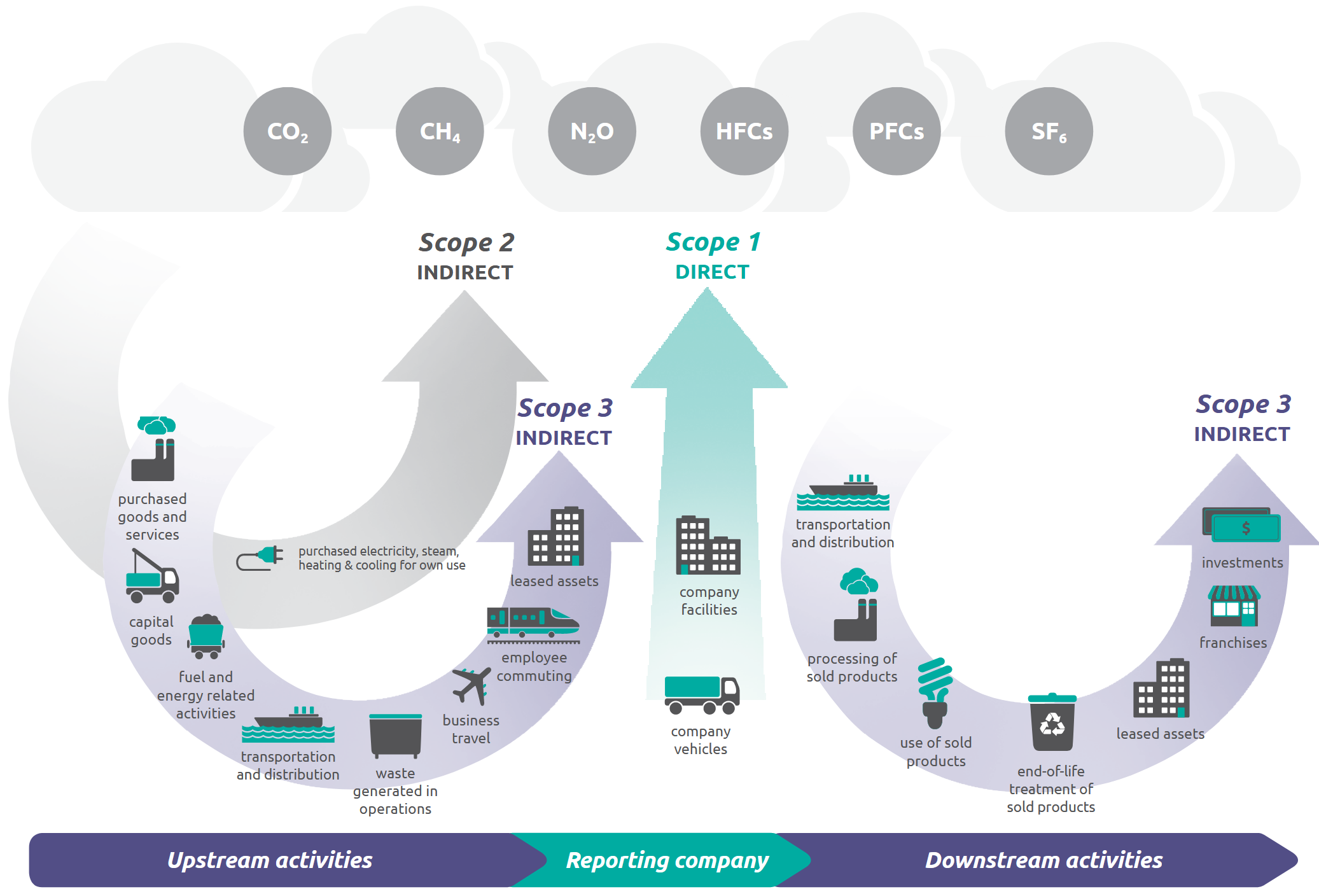

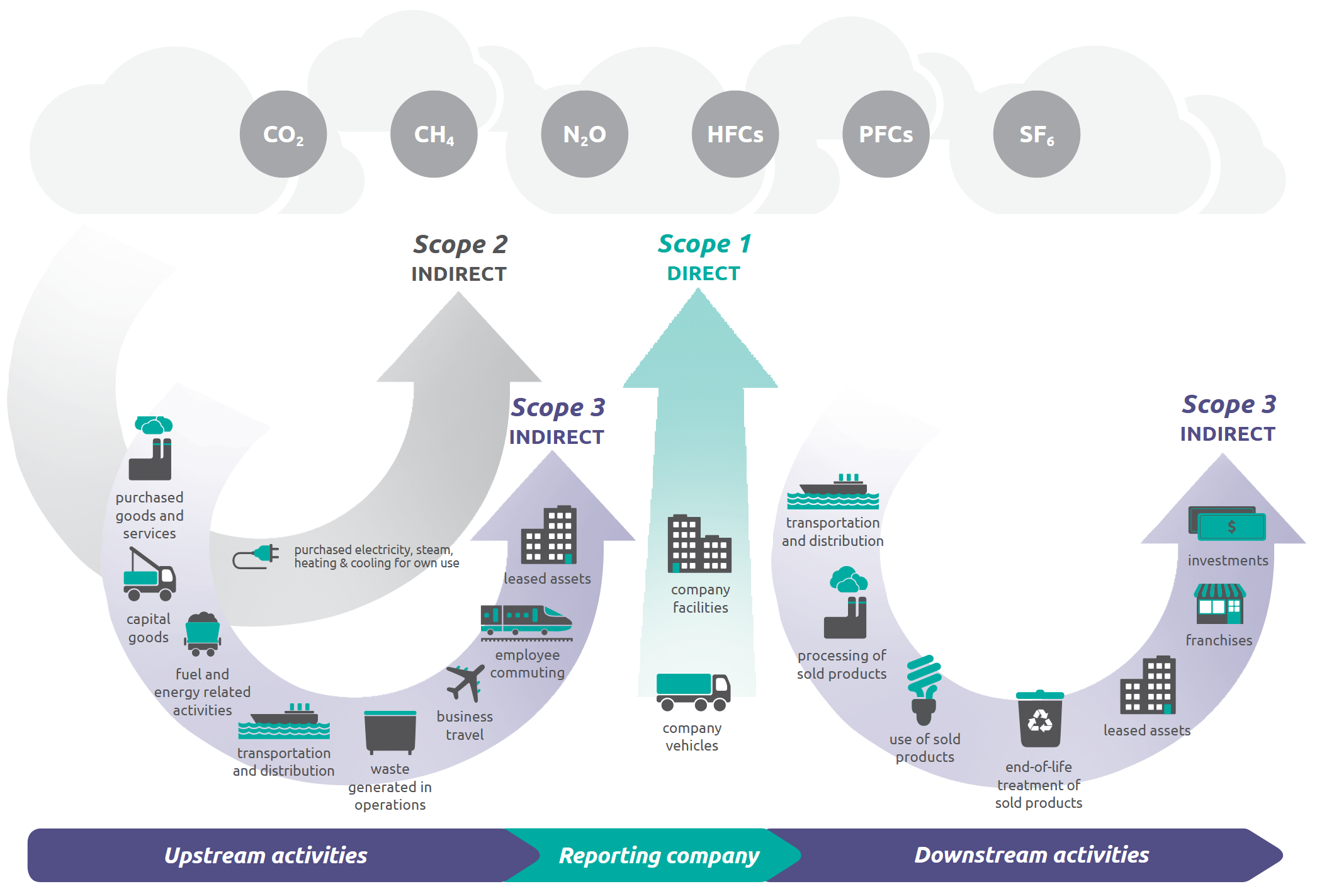

Overview of GHG Protocol scopes and emissions across the value chain

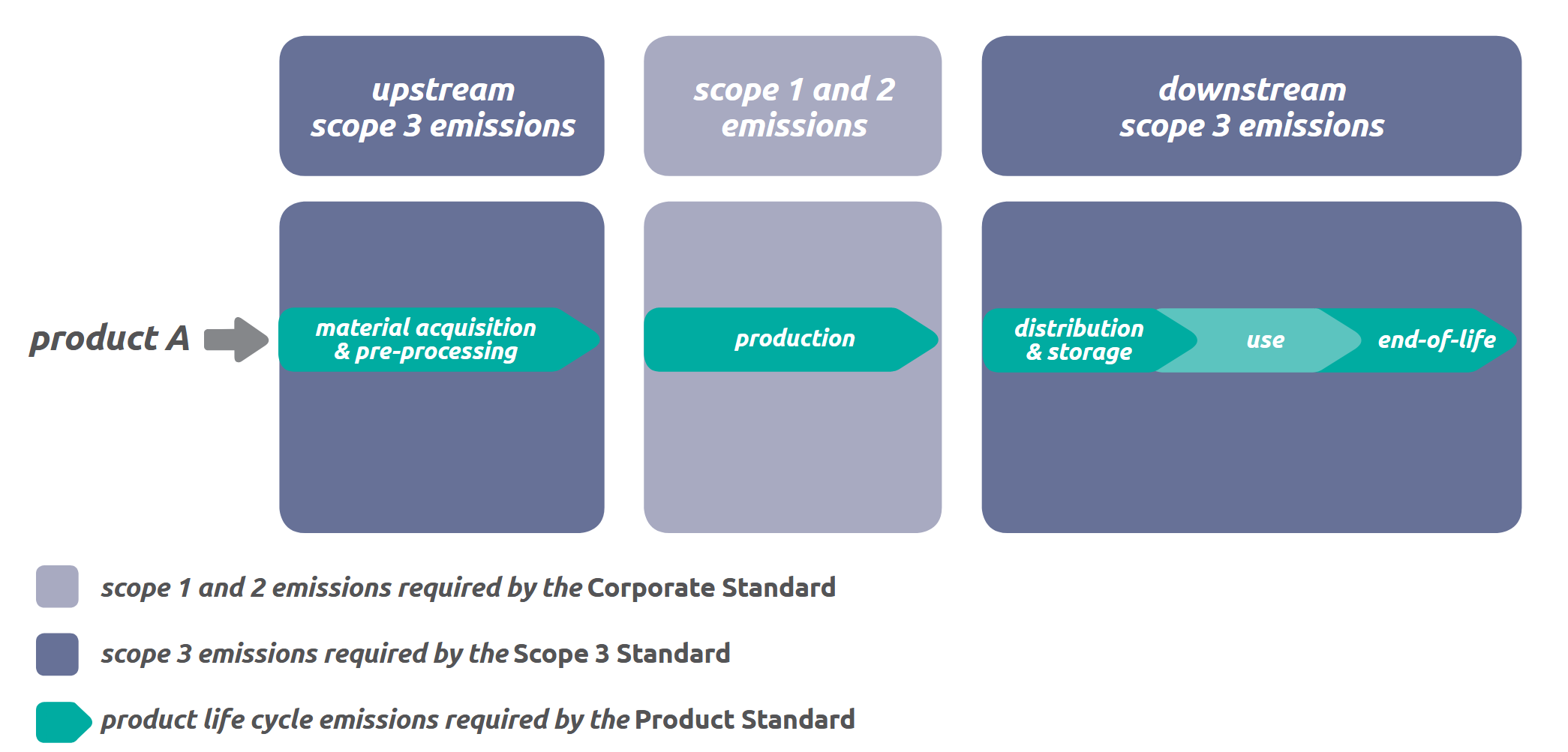

Relationship between a scope 3 GHG inventory and a product GHG inventory (for a company manufacturing Product A)

Direct emissions are included in scope 1. Indirect emissions are included in scope 2 and scope 3. While a company has control over its direct emissions, it has influence over its indirect emissions. A complete GHG inventory therefore includes scope 1, scope 2, and scope 3.

By allowing for GHG accounting of direct and indirect emissions by multiple companies in a value chain, scope 1, scope 2, and scope 3 accounting facilitates the simultaneous action of multiple entities to reduce emissions throughout society. Because of this type of double counting, scope 3 emissions should not be aggregated across companies to determine total emissions in a given region.

Overview of the scopes

This standard divides scope 3 emissions into upstream and downstream emissions. The distinction is based on the financial transactions of the reporting company.

- Upstream emissions are indirect GHG emissions related to purchased or acquired goods and services.

- Downstream emissions are indirect GHG emissions related to sold goods and services.

Overview of GHG Protocol scopes and emissions across the value chain